ECB Rates Analysis

ECB Rates jumps again to a 15-year to-

Report and analysis released by HSBC

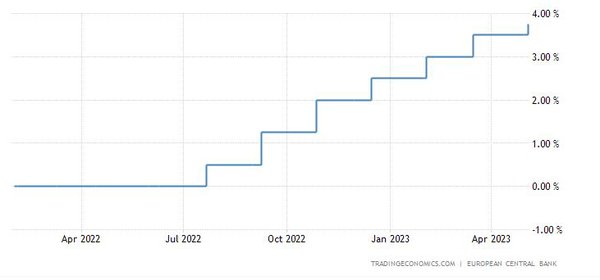

The ECB raised its key policy rates by 25bps in May, taking the deposit rate to 3.25%. This marked a slowdown in the pace of rate rises, after six consecutive hikes of 50 or 75bps.

The outcome was in line with our expectation and broadly in line with the market (which priced in +29bps ahead of the meeting) and consensus (where 43 out of 55 economists surveyed by Bloomberg expected a 25bp hike).

The policy statement noted that "the inflation outlook continues to be too high for too long" and that "headline inflation has declined over recent months, but underlying price pressures remain strong".

It stated that "future decisions will ensure that the policy rates will be brought to levels sufficiently restrictive to achieve a timely return of inflation ... and will be kept at those levels for as long as necessary."

ECB rate decisions

The Governing Council (GC) said it "will continue to follow a data-dependent approach to determining the appropriate level and duration of [policy] restriction".

Perhaps in light of the recent ECB Bank Lending Survey (Higher rates, not market turmoil, having an impact, 2 May 2023), however, the ECB now thinks that "past rate increases are being transmitted forcefully to euro area financing and monetary conditions".

The ECB also announced that it "expects to discontinue the reinvestments under the APP as of July 2023", in line with our expectations. This means that from Q3, the APP portfolio will shrink at an average pace of EUR25bn per month this year, amounting to an additional EUR60bn of QT relative to the pace in Q2 (Chart 1). For 2024, that would imply an average of around EUR30bn of APP shrinkage per month.

PEPP reinvestment will continue "until at least the end of 2024" and the roll-off of PEPP "will be managed to avoid interference with the appropriate monetary policy stance". Also, the GC said it will "regularly assess" how the repayments of the TLTROs will affect its policy stance.

Implications of rate hike by the ECB

As in March, the ECB has said that inflation is projected to remain "too high for too long" and offered no explicit policy guidance other than re-iterating the importance of a data-dependent approach. However, the fact that it said it will ensure that policy rates "will" be brought to sufficiently restrictive levels suggests it is not done yet. This chimes with our view that there will be another 25bp rate rise next month, with the risk of hikes continuing into July.

The announcement of a faster pace of QT also seemed likely. Calls to start shrinking the ECB's balance sheet faster have grown louder. Isabel Schnabel argued (27 March) that shrinkage was warranted for three reasons: (1) to restore policy space; (2) to mitigate unwanted side effects; and (3) to withdraw policy accommodation.

With faster QT providing some degree of monetary tightening, this was no doubt another factor in slowing the pace of rate hikes. Indeed, more hawkish GC members that might have preferred another 50bp hike may well have compromised in order to ramp up QT.

Moreover, the tightening impact of balance sheet reduction may be significant. In a speech on 16 February, Chief Economist Philip Lane argued that a EUR1trn balance sheet reduction over three years could take a cumulative 0.3ppts off inflation. This is roughly the same magnitude of the peak inflationary impact of a 100bp rate rise. Put simply, Mr Lane's analysis suggests the total impact on inflation of a EUR1trn balance sheet reduction could be about the same as four 25bp rate hikes.

ECB Balance sheet

With the announcement of APP reinvestment stopping from July, this implies about EUR0.5trn of balance sheet reduction by end-2024 from the APP alone. But factoring the TLTROs, where EUR1.1trn is set to expire between June 2023 and December 2024, total balance sheet reduction between March 2023 and then end of next year could be around EUR1.5trn. Unless some of the TLTRO funds are rolled - and the ECB is clearly keeping its options open there - that implies significant additional tightening based on Mr Lane's calculations (which would imply a 0.5ppt reduction in inflation, other things equal).